Most days, the stock market doesn’t see high highs or low lows. Generally speaking, indices like the S&P 500 gain or lose less than 1% a day. Every once in a while though, the market will experience periods of unprecedented sharp downtrends or upward trends. This is what the investing world refers to as volatility, and can often be the key to investor success.

In this article, we’ll consider the following:

- What is market volatility?

- What is driving this volatility now?

- What are the effects of inflation on consumers?

- What are the effects of inflation on investors?

- How should investors manage volatility?

- Best practices

- Takeaways

- What is market volatility?

Volatility is an investment term that describes when a market or perhaps maybe a particular asset experiences periods of unpredictable, and sometimes sharp, price movements. This may lead investors to wonder how to deal with volatility, and how they can continue to manage their securities in uncertain times.

Volatile markets come with the territory, it’s important to get comfortable with it, and build portfolios that allow investors to hold the fort or even excel in the somewhat capricious environments of the markets. But before we get into how investors should manage volatility, let’s dive into the reasons behind the recent downturn in the market.

- What is driving this volatility now?

We’ve seen some market volatility in the recent weeks of 2022. Looking at the US, the S&P 500 has dropped nearly 10% from its latest high. Meanwhile, the Nasdaq, which is a tech heavy index, has experienced a double-digit drop year to date, in what seems to be the worst start to a year for the index since 2008.

You might be asking, “what’s driving this volatility?” Well, in this case, it’s been record high inflation figures, investors’ expectations of the Fed’s aggressive monetary policy measures, the latest developments in Ukraine, as well as a hefty dose of panic selling.

Spikes in general price levels first became of interest during the Spring of 2021. The Fed listed three main reasons for that:

- Base effects: prices dropped significantly in 2020 due to government-imposed lockdowns globally in an attempt to flatten Covid infections, so any year-on-year comparisons are bound to seem excessive as the economy gradually opened up.

- Supply Chain: very much tied to the pandemic as well; supply of goods were limited due to shortages, overwhelmed supply routes, and idle ports. While supply takes time to adjust, demand however is much faster in moving up or down, which resulted in an imbalance between supply and demand.

- Labour issues: millions of Americans lost their jobs in the past few years, in what was the sharpest labour contraction on record, decreasing the amount of goods produced. As demand picked up starting the second half of 2020, mainly due government stimulus checks, this led to a lower level of produced goods being chased by large sums of money.

In summary: a partially halted economy combined with limited supply, and labour constraints created an upward pressure on prices for common goods and services.

- What are the effects of inflation on consumers?

As prices increase, individual purchasing power drops, meaning dollars afford less than what they used to. We experience this when paying bills, buying real estate, or even buying a car. Inflated prices signify that goods and services will be allocated larger spending in a person’s budget.

If wages were to mimic increases in the general price level, though, inflation should typically not impact spending.

However, if inflation levels were to reach higher highs than what we’re used to – this could put employers in a tricky situation. If an employer were to bump wages in order to deal with this inflation, the additional cost would consequently be passed on to the consumer. How? Well, with goods now being more expensive, and workers (who are also consumers) earning more, it’s still not an ‘earn more, pay less’ situation. In fact, workers and consumers are earning more and also paying more. Now the pattern becomes clear, as in: how do we cap inflation if we follow the cycle to? This is known as the wage-price spiral. A case of the wage-price spiral was seen in the ‘70s, where inflation reached double digit numbers in the US.

- What are the effects of inflation on investors?

A stock is a claim on a company’s future cash flows. As inflation picks up, this should result in higher earnings for companies, thus having a positive impact on equity prices. However, this is not long-lasting, since a spike in price levels would take a toll on consumers, cost of business, as well as the overall economy.

When inflation moves from a “low-and-slow” state to “boiling,” this pushes officials to cease expansionary activities, and take certain measures to cool down the economy. This can be done via several monetary policy measures, which aim to reduce money supply. One of these measures include increasing interest rates with the objective to encourage some investors to place their funds in interest-linked accounts. Keep in mind, this is not for everyone, and investing in such environments depends on the risk profile and appetite of the investors.

As mentioned earlier, wallets of consumers are impacted if wages do not follow, meaning that a decrease in overall spending will slash company earnings, and impact valuations.

Additionally, inflation creates uncertainty for certain emotionally-invested investors, which pushes both businesses and investors to postpone decisions around investment opportunities. This is what leads us to how you, an investor, can manage your investments during volatile times.

What can we expect?

If we zoom in on the U.S. market specifically, the Fed has switched their positioning regarding inflation throughout 2021. What was first assumed by many as ‘transitory”, some are seeing as a challenge to the health of the economy. Analysts are expecting three rate hikes to take place in 2022, in an effort to lower inflation.

The actual response will depend on several factors. One that comes straight to mind for many is the effect of Omicron (and other possible strains), the economy’s operational capacity, or the efficacy of vaccinations over time.

- How should investors manage volatility?

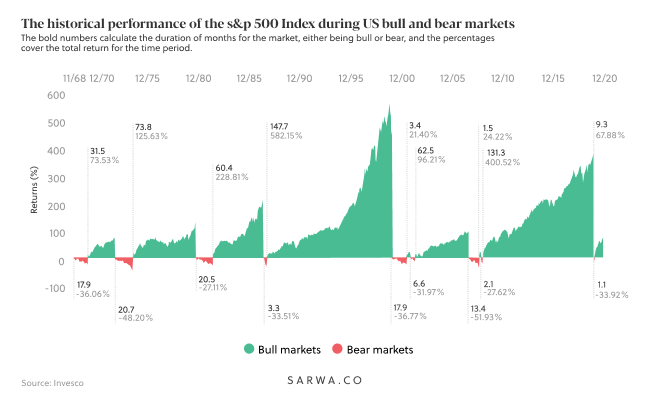

Markets are cyclical by nature, with periods of expansionary or contractionary trends. Volatility and market corrections are part and parcel of investing. However, history has shown that volatility is short lived, and over the long term markets recover and flourish. Judging the viability of your investment decisions based on a short-term period probably won’t lead to the returns you’re looking to see. Let’s have a look at the periods of strong market activity, and periods of poor performance below:

You will note that bear markets, which are periods when the markets experience a drop of 20% or more from their recent highs, are short in nature. Recent examples would be the 2008 financial crisis and the onset of Covid and its impact on the markets in March 2020. However, bull markets, which are periods in which the market is rising, last significantly longer, and investors who remain invested during those times of volatility were rewarded for their patience.

With all the information sources available at our fingertips, the temptation is there to react to short term volatility by exiting from the market in hopes of coming back when markets stabilise. This type of short-term focused investing has proven to be far from sustainable over time. Exiting and re-entering the market has historically had a negative influence on an individual’s investment returns. Let’s take a look at the graph below. This shows what the impact would have been if an investor exited during a bear market and re-entered during a bullish trend. We highlight an example of a $10,000 investment in the S&P 500 between January 3rd, 2000 and December 31st, 2019. A time period that experienced considerable movements of volatility (2000 Dot Com Bubble, 2008 Financial Crisis).

This chart illustrates that had you remained invested during this time, in spite of the volatility that ensued, your portfolio returns would have been significantly higher than taking the approach of exiting and re-entering the market at a later date. Just missing the top 10 days of market growth between 2000 and 2019 is associated with an average yearly underperformance of 3.62%. Timing the market has shown to not be effective, and hurts the performance of your portfolio. This is where the adage of “time in the market versus timing the market” comes from.

6. Best Practices

We believe that a passive investment approach is the best way to build long-term wealth. Instead of falling into the eventual trap of market timing, efforts would be best spent on investing in a globally diversified portfolio, with a mindset of growing alongside markets throughout your horizon, rather than focusing on outperformance in the short-term. Focusing your efforts on reducing your investment fees, choosing the most appropriate risk level for you, and having a goal based approach to your investment decisions has been the most beneficial to investors. It works!

Now, considering the current volatility that we are experiencing, there three ways we recommend you approach your investment decisions:

Seizing An Opportunity

Market prices have retracted to levels we have seen in late 2021. This presents an opportunity for some investors with the right risk profile to buy in at lower price levels. If you have your emergency reserves set aside, your debt obligations (if any) addressed, and you have additional capital sitting idle, this could be an opportunity to capitalise on the recent market downturn. Injecting funds when markets are on a downward trend is an efficient way to lower your average purchase price, increasing your potential returns over your investment horizon.

Do Nothing

You read that right. Do nothing. Remaining invested through market volatility is also a viable approach. Doing nothing may feel risky, but history has proven the opposite time and time again. Avoiding rash emotional decisions and maintaining discipline have a positive impact on the long term growth of your wealth.

Review Your Risk Profile

If the volatility levels we are seeing are causing some concerns, consider reviewing your current risk profile. Since we know to expect volatility during your investment journey, is the risk profile you currently have appropriate for you? If the current market movements are causing you to reconsider your investment decision, to the point of exiting, consider lowering your risk profile to a level that you are comfortable with. This way, you are still participating in the markets and putting your money to work.

Adopting a hands-off, long-term, passive approach has historically been the best way to ride through these volatile times. Combining this mindset with a globally diversified portfolio, without taking directional bets, enables you to spread your risk while maximising your long term growth – this is at the core of our portfolio construction methodology. Remain invested, focus on the long term, and ignore the short term “noise” to enable you to achieve your financial goals. When confronted with volatility, the best approach is to zoom out and see the bigger picture of how markets have performed over the past market dips. Consider the opportunities that lie in volatility, and if needed, reassess your current risk profile so as to remain invested over the long term.

We’ll leave you with this illustration: focus on the long-term, not the short-term vision.

Nothing compares to smart, responsible and hassle-free investing. So stay calm, stay composed, and stay invested!

Past performance is no guarantee of future results. Historical returns, expected returns, and probability projections are provided for informational and illustrative purposes, and may not reflect actual future performance. All investing involves risk, including the possible loss of money you invest.

7. Takeaways

- Market volatility in the market is normal. It comes with the territory.

- Focus on your long-term approach, not the short-term.

- Don’t let your emotions get the best of you. Stay calm.

- Volatility is an opportunity to make smart investment decisions.

- Block out the noise. Diversify, and stay invested!