[‘Investor Journeys’ is a new series that uncovers how Dubai investors are uniquely approaching money and investing in our great city.]

Skye Nguyen has followed a longer road than most in her investment journey.

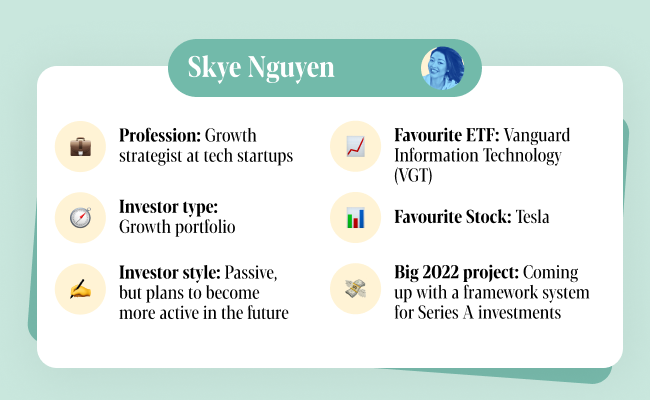

The Dubai-based growth strategist is originally from Vietnam, and has acquired enough financial confidence to start investing in cryptocurrency and rattle off her favourite ETF, but she grew up in a setting where money was viewed as a scarcity.

“My family is from a communist country, and I grew up with the impression that there’s only enough money for surviving, and not for saving or investing,” Skye remembers. “The first time I heard the word ‘investing’ wasn’t until when I was 17.”

Like many women that are new to investing, Skye was risk averse. Ironically, this natural risk aversion was deepened by an early part-time job as a stock trader.

“I never invested my own money, but I came to see stock trading and the markets as a very high risk thing. I saw my clients do crazy things with their money in the stock exchange,” she recalls.

The key to overcoming her natural (and common) anxiety was learning how to budget and understanding more about herself, especially her emotions.

“I’m at the stage now where I kind of got the financial literacy, even though I would not call it intelligence. But I know the importance of how to budget, how to spend money wisely, and what are my narratives and emotions around money,” she says.

Along the way, Skye has developed a unique approach to budgeting, one that fits the specific risk-averse tendencies of women, as well as meets some natural penchants for building a secure nest egg.

Sarwa wanted to hear more about Skye’s unique approach to budgeting, as well as why she thinks that women should NOT invest like men.

And she may be right – just read on to hear why.

What were conversations about money like when you were growing up in Vietnam, and how did that impact you?

Money wasn’t necessarily a taboo in my family, but rather more of a concern that there wasn’t enough beyond the coming month. I was not hyper-aware of the cost of things, but asking for toys or nice clothes was off limits.

I’m just waking up from the impact – I subconsciously believed that I only have enough to spend for the month (paycheck to paycheck). This was how I thought up until a few years ago. Today, I’m a lot more (emotionally) balanced when it comes to money, and have learned a lot from a Japanese author called Ken Honda.

How would you classify your relationship with money today?

Today, I have mentally divorced myself from the paycheck-to-paycheck narrative as experienced in my childhood story.

Now I consider money as growth capital and myself as a high-growth startup. I’m spending more on savings/investing and on things that move me forward and increase my income to put back into savings and investment.

How have your spending habits changed since you started investing?

I think the best habit that I have learned is how to classify and use money to achieve your goals. Since I started investing, I now classify money into three categories: past, present and future.

For example, I will classify expenses such as credit card debt or student loan debt as an expense that is from the past, the present is for my current living expenses, and the future is for savings and investing into the future me.

Future expenses can include what kind of educational courses I need to take, or savings and investment accounts that I need to put money into every month.

Importantly, I’ll make sure that I spend a lot more on the future compared to the past, and I’ll spend a decent amount on the present because I don’t want to live a constrained life. However, what is key for me is to not beat myself up about the past.

Tell us more about this budgeting approach. How much do you allocate for past, present and future?

I allocate 50% of income to the future, 30% to the present, and 20% to the past.

50%! That’s quite ambitious.

That is because I’m a growth strategist for startups, so I kind of allocate money to myself in the same fashion that I would allocate to a growth startup.

The idea is simple: I want to move away from whatever that has happened in the past. For example, if someone finds that they are going through a bitter divorce, I would tell him (or her) to just put it in the past and don’t attach negative emotions to those events and expenses.

Let the past be in the past, and then allocate more money towards the future.

Should women learn to invest as much as men do?

I agree that women should participate more in investing, but not to invest like men. In fact, I don’t think women should invest like men at all.

I think I’m generalising here, but I think women naturally have different risk appetites and they also have different life priorities compared to men.

For women, it’s a lot about security. So they should identify and pick an investment strategy that fits their priorities. This is why my budgeting approach helps to allocate half of income to creating a secure future.

What advice would you tell women who haven’t started investing yet?

Women don’t see themselves as investors and women tend to not see themselves as someone who handles money. I think this is simply because of a lack of financial education, plus the stereotype is that the man in the house should be the person that handles big purchases and investments.

Of course, society doesn’t function this way anymore. But the narrative is so engrained generation after generation that it naturally strips away the confidence of women to even start investing.

These days, the toughest hurdle to overcome is actually to look and find an investment platform that you can trust, and then just put in a little bit of money every month. This is to help build a habit, but not go too far. Don’t go into things like, “Okay, I’m gonna go from zero experience to put all of my assets into crypto” overnight.

Do you think women should also consider crypto even though it’s high risk?

I have actually included crypto in my Sarwa portfolio. I won’t say that I have really gotten into it yet. But I’m okay with having the 5% allocation in my portfolio.

Finally, what did Covid-19 teach you about your approach to money?

Like many, I’m still shaping my investment and life thesis around the impacts of Covid-19.

I haven’t fully come to the conclusion yet, but I have become a lot more self reliant in both investment and my career. I have built up more knowledge and skills that revolve around me while reducing dependencies on external factors. If anything, Covid-19 has shown us that things can change overnight.