Understanding the difference between saving vs. investing plans is crucial when it comes to personal wealth building.

Often, this means learning to strike a balance that best fits your unique appetite for risk.

Since balancing both risk and return are important factors in making investment choices, it’s common to hear that many new investors are torn between how to allocate their money for saving and investing, which makes the saving vs. investing debate a perennial one.

A common question many ask is “how much should I keep in savings vs investments.”

This answer always depends on the individual, as we’ll explain.

Ultimately, you’ll need to navigate the risk and return divide associated with investing in the stock market versus preserving some capital for emergencies. How you divide this up will depend on your lifestyle and monthly costs, as well as your ambition to reach future financial goals.

In this article, we will weigh into this debate by considering how saving is different from investing and the best way to approach the two in financial planning.

We will consider:

- Saving vs. investing: Definitions and differences

- Investing and wealth building

- Saving and the preservation of money

- Navigating saving and investing

- Diversification and the minimisation of investment risk

- How to invest in the UAE

[Do you want to create an investment portfolio that will help you achieve your financial goals? Register with Sarwa Invest or learn more here about how to invest successfully in the UAE.]

1. Saving vs. investing: Definitions and differences

Let’s get some simple definitions out of the way.

Saving is the setting aside of a sum of money for later use (usually in an interest-yielding account) where it has a lower risk of losing its value and can be easily accessed. [Check out Sarwa Save, a high-yield savings option with an annual return rate of 3%.]

The primary feature of saving is not the act of setting money aside, but where the money is set aside. Common instruments for saving money include traditional savings accounts, high-yield savings accounts, money market accounts, money market mutual funds, and even halal savings accounts, like the Sarwa Save Halal.

All these instruments for saving yield little return to the saver but they are low-risk, which means they should only be used for short-term goals, like emergency funds, saving for a trip, saving to buy a house, etc.

In essence, they are low-risk and low-return instruments.

Importantly, funds saved through these channels can be easily accessed when they are needed. This makes savings the ideal tool for creating personal emergency funds.

Investing, on the other hand, is the setting aside of funds in wealth-building instruments that can potentially create good returns for the investor over a period of time.

In other words, investing also involves the setting aside of money; what differs is where the money is set aside. Investors set aside funds in wealth-building instruments like stocks, bonds, mutual funds, ETFs, currencies, commodities, etc.

Unlike instruments for saving, these investing channels provide higher returns but also come with higher risk of losing money.

Having defined saving and investing, let’s highlight some differences that should have become obvious by now:

- Goal: The goal of saving is to preserve a certain amount of money while earning minimum interest on it. On the other hand, the goal of investing is to build wealth by growing a certain amount of money.

- Accessibility: Savers want their money to be easily accessible when they need it while investors want their money to grow as much as possible (which means a long-term horizon).

- Instruments: Savers make use of low-risk and low-return instruments like savings accounts and money market accounts. Investors use wealth-building instruments like stocks, bonds, and mutual funds.

For example, while the average interest rate (annual percentage yield) for savings accounts in the US has been less than 0.20% since 2010, the S&P 500 Index (an index of the stocks of the largest 500 companies in the US) has returned an average of 9.69% between 2010 and 2022.

Despite their differences, there are also similarities between saving and investing:

- Setting money aside: Both saving and investing includes taking away money from a checking account and setting it aside to achieve a goal.

- Earning interest: While investing yields higher returns, both saving and interest earn interest.

Consequently, a saving vs investing Venn diagram will overlap at these two points: setting money aside and earning interest.

Now that we understand what saving and investing are all about, let’s go on to answer the question, “how much should I keep in saving vs investments?”

We’ll do this by considering where investing is valuable and where saving is valuable.

2. Investing and wealth building

As we have said above, investing is the engine of wealth building.

“How many millionaires do you know who have become wealthy by investing in savings accounts?” famously asked Robert Allen, author of Cracking the Millonaire Code, in an attempt to showcase the superiority of investing.

We all need to build wealth to secure our future and to achieve other financial goals (buy houses, send our children to school, start businesses, and leave wealth for the next generation).

But building wealth requires a high rate of return compounded over a period of time. An annual percentage rate of 0.12% will not help anyone build wealth. A $1,000 in such a savings account will become $1,012 in 10 years even with daily compounding.

Not so exciting, is it?

However, if we had switched to stocks and bought an S&P 500 fund (assuming the average returns of 9.69% is consistent throughout), your $1,000 would become $2,635 in 10 years.

The difference, as they say, is clear.

Therefore, while investing can be riskier than saving, it generates better returns and is much more appropriate tool for wealth building.

Saving might be safe, but only focusing on savings will mean we will have to work all through our lives and leave many of our financial goals unachieved. Since most of us don’t want that, we will have to invest in the financial market by buying stocks, bonds, mutual funds, and ETFs, among other assets.

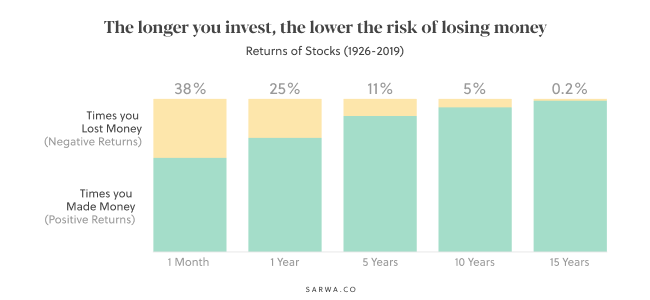

Moreover, the risk associated with investing can be minimised. For example, a study by the Center for Research in Security Prices has shown that the longer you stay invested in the market, the lower the risk of losing money becomes.

How long-term investing reduces risk

Therefore, instead of running away from investment, you should embrace it for its high returns and use long-term investing to minimise risk.

3. Saving and the preservation of money

While investing is crucial for wealth building, saving is also beneficial for the preservation of money, especially for emergency needs.

As much as using money to build wealth is preferable to preserving it, there are instances where the latter becomes essential.

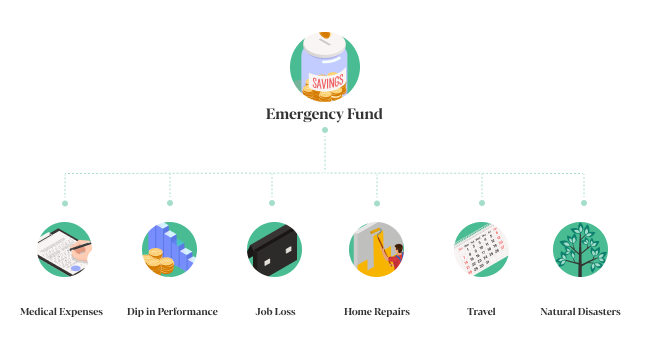

Emergency funds

First is the issue of handling emergencies.

Emergencies can be unexpected and unplanned events that require you to spend money you have not budgeted. Examples include a car breakdown, unplanned travel, job loss, funeral expenses and unplanned medical expenses.

If you invest all of your money without creating savings for these expenses, then you will be in a difficult situation when emergencies occur.

Investment assets are more volatile (with lots of ups and downs), so there is a possibility that the market may be in a downturn when emergencies arise. This means that you will have to liquidate your asset at a loss if you want to meet that emergency.

Also, by the time you are ready to return the amount you withdrew, the market might be in an upturn, which means it will cost more to replace the asset you already sold at a loss. Throw in the difficulty and delay (some investment platforms might require that you wait for 2-3 business days) you might experience trying to withdraw money from your investment account and it’s a big mess.

The other option is to borrow money to meet those emergencies. But that means paying loan interest rates that can become a strain on your future income.

To avoid these two unideal situations – liquidating your investments and borrowing money – you can start an emergency fund, which will allow you to save money for such emergencies.

Made in a savings account, the emergency fund will not yield high returns but your money will be preserved and, more importantly, easily accessible when emergencies arise. Consequently, you won’t have to borrow or liquidate your investments.

Short-term financial goals

A second instance where saving is important is when you have to meet short-term financial goals. If you have to buy a TV in three months, make a downpayment on a mortgage in six months, or purchase a car in the next nine months, it is better to save money towards these goals than investing for it.

As we saw in the chart above, the longer you stay in the market, the lower the risk of losing your money, and vice versa. If you put money you need to use in three months into the market today, the next three months might turn out to be a bear market. This means by the time you sell your stocks or ETFs, you will have less money than you put in.

Take 2022 as an example. The S&P 500 Index opened at $4,796.56 at the beginning of the year. At the time of writing, it is now trading at $4,305.20. If you had put money for the downpayment on your mortgage there, it would have lost value due to the bear market.

On the other hand, if you had put the money in a savings account, it would have grown, even if it is by a small margin.

In other words, money that you need to access within a year is better preserved through saving rather than investing.

Investing should be for money you are willing to use to build wealth for the medium and long term.

4. Navigating saving and investing

The budget is the foundation of financial planning.

So, when it comes to the saving vs. investing question, it is best to explain how everything we have said thus far will play out in a budget.

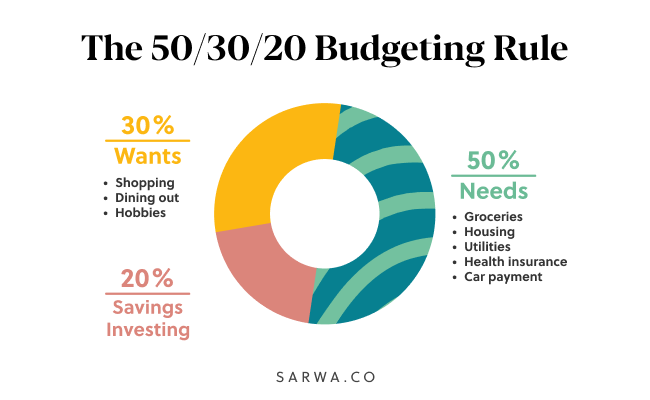

For this section, we will consider the 50/30/20 rule, which is a simple and popular budgeting system and the bedrock of the monthly investment plan. In this system, 50% of your income goes to your needs and 30% to your wants. The remaining 20% should be for saving/investing.

So, should the 20% be for saving or investing?

Saving and investing without debt

If you are free from debt, your goal should be to first set up an emergency fund worth three to six months of your living expenses (wants plus needs). If those add up to $5,000 per month, for example, you need an emergency fund worth between $15,000 and $30,000.

Many financial advisors recommend that you take the upper limit for more safety.

After setting up your emergency fund, you can start investing 20% of your income every month. However, if you have short term financial goals, you will need another savings account where you can commit such funds.

In essence, if you are without debt, you should first use the 20% of your income to start an emergency fund. After that, you can begin investing as well as saving for short-term financial goals.

Saving and investing with debt

If you have debts where interest accrues on the unpaid balance (credit card debt, car loans, and other consumer debt) at the end of every month, paying those off should be a priority. These are different from “good” debts like mortgages which are for the building up of your net worth through a home, which is an asset (payment for which will be part of your needs).

How should you proceed if you have any of these “bad” debts?

First, build your emergency fund a bit. If you don’t build any emergency fund at all and concentrate on paying off debts, you might be forced to even take up more debt when an emergency arises. So, you can start by building half of the total funds you want in your emergency fund.

Second, start paying off your “bad” debt through the debt snowballing system. This system helps you tackle smaller debts and use that confidence to move on to bigger ones until you are free.

Third, complete your emergency fund. Now you can add the extra cash to make up your emergency fund.

Fourth, start investing. Now that you have taken off “bad” debts from your books and completed your emergency fund, you can start building wealth.

Fifth, save for short-term financial goals. When you have to achieve short-term financial goals, remember to save instead.

5. Diversification and the minimisation of investment risk

In a previous section, we mentioned how long-term investing can reduce investment risk.

Another tested way to reduce risk is diversification.

By building a diversified portfolio of zero-correlated, negatively-correlated, or less positively-correlated assets, you can minimise your risk and maximise your returns. For example, investors have traditionally added bonds to stocks to reduce overall portfolio risk since bonds are less risky and are oftentimes less positively-correlated to stocks – among the riskiest of the assets.

Recently, ETFs have provided the best option for diversification.

Apart from the fact that a single ETF is already diversified, you can add many zero-correlated, negatively-correlated, or less positively correlated ETFs together in a portfolio to reduce risk more significantly. This diversification can occur by industry (healthcare, finance, consumer staples, etc.), market (emerging and developed), market cap (large, small, and mid), and asset class (bonds, stocks, REITs).

The key point here is that with diversification, you can invest to build wealth without worrying too much about the high risk of investment assets.

6. How to invest in the UAE

For wealth-building, you can use Sarwa Invest. With Sarwa Invest, investors can build wealth through a diversified portfolio of ETFs. This portfolio is designed with the Nobel Prize-winning Modern Portfolio Theory and its aim is to help maximise returns and minimise risk.

Sarwa Invest portfolios are also created to match your unique time horizon, risk tolerance, and financial goals.

You can also automate your investing straight from your bank account. This will help you to pay yourself first when you receive your income and avoid the temptations of spending what you should invest. Sarwa Invest also allows you to reinvest your dividends to further increase your returns through compounding.

[Do you want to build wealth through smart investing? Register for Sarwa Invest to get a diversified portfolio of ETFs that will help you achieve your financial goals.]

Takeaways

- While the goal of saving is to preserve money for future use, the goal of investing is to use money to build wealth.

- Saving uses low-risk and low-return instruments like savings accounts and money market accounts while investing uses instruments like stocks, bonds, mutual funds, and ETFs that yield more returns but with more risk.

- Saving is appropriate for building emergency funds and meeting short-term financial goals, while investing is appropriate for building medium- and long-term wealth.

You can reduce the risk inherent in investing through diversification and long-term investing.