Tens of thousands of UAE residents have lost their life savings to bogus investment scams and get-rich-quick schemes, according to a 2024 report by Khaleej Times.

This situation has not changed much, leading Dubai Police to issue a warning against “fraudulent investment schemes circulating on digital platforms and social media.”

The truth remains that building wealth requires consistent investing, and shortcuts can only lead to financial ruin.

Rome was not built in a day. The journey of a thousand miles begins with a step. Slow and steady wins the race, and so do investors who start systematic investment plans (SIPs), such as by investing $1,000 per month for five years.

You may have heard that consistent investing builds wealth, but you have not seen how it works. In this article, we will correct that by showing you real numbers.

We’ll cover:

- How consistent investing in a SIP builds wealth: Examples for passive investors

- How consistent investing in a SIP builds wealth: Examples for active investors

- How to construct and execute your SIP in the UAE

Do you want to learn more about the best way to invest money in the UAE? Sign up now for Sarwa’s Fully Invested newsletter for insights on how to take advantage of trends in the global economy.

1. How consistent investing in a SIP builds wealth: Examples for passive investors

If you are an investor who doesn’t have the time or skills to research individual stocks and other assets, you may prefer to go the passive route.

You can do this in two ways: invest in an S&P 500 index fund (or ETF) or subscribe to a digital wealth management platform (also known as a robo advisor).

Investing in an S&P 500 fund

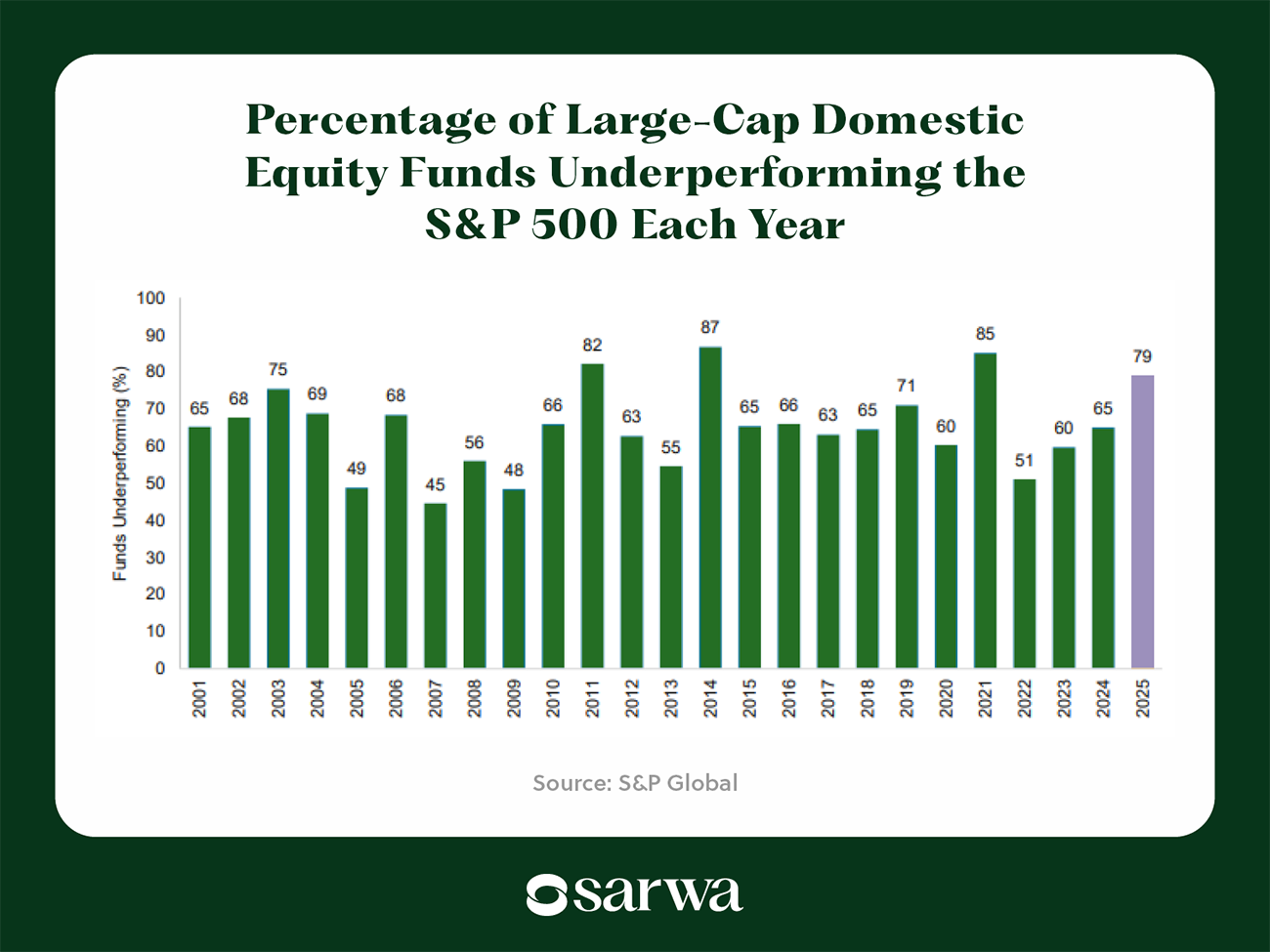

Over the past years, analysts and researchers have shown that mutual funds that actively help people manage their money actually end up underperforming their benchmark indices, usually the S&P 500 Index.

To pick a single example, 78% of large-cap equity mutual funds in the US underperformed the S&P 500 Index in 2025, according to a survey by S&P Global, a global financial services firm.

Source: S&P Global

As a result, financial experts and accomplished investors have advised retail investors to stick to tracking the performance of the S&P 500 Index.

In other words, instead of paying huge fees to fund managers who fail to outperform the S&P 500 Index, it’s better to pay very low fees to buy funds that track the S&P 500 Index. Passive investors who do this end up posting higher net returns than most fund managers.

“An ‘average Joe’ has the ability to surpass over 90% of money professionals by investing in index funds,” according to Elie Irani, a personal finance educator, in his interview with Sarwa. “Beating the market is extremely hard to repeat.”

Interestingly, this is a view shared by stalwarts like Warren Buffett (who placed a bet on passive investing), Ray Dalio, Mark Cuban, and Jonathan Clements, among others.

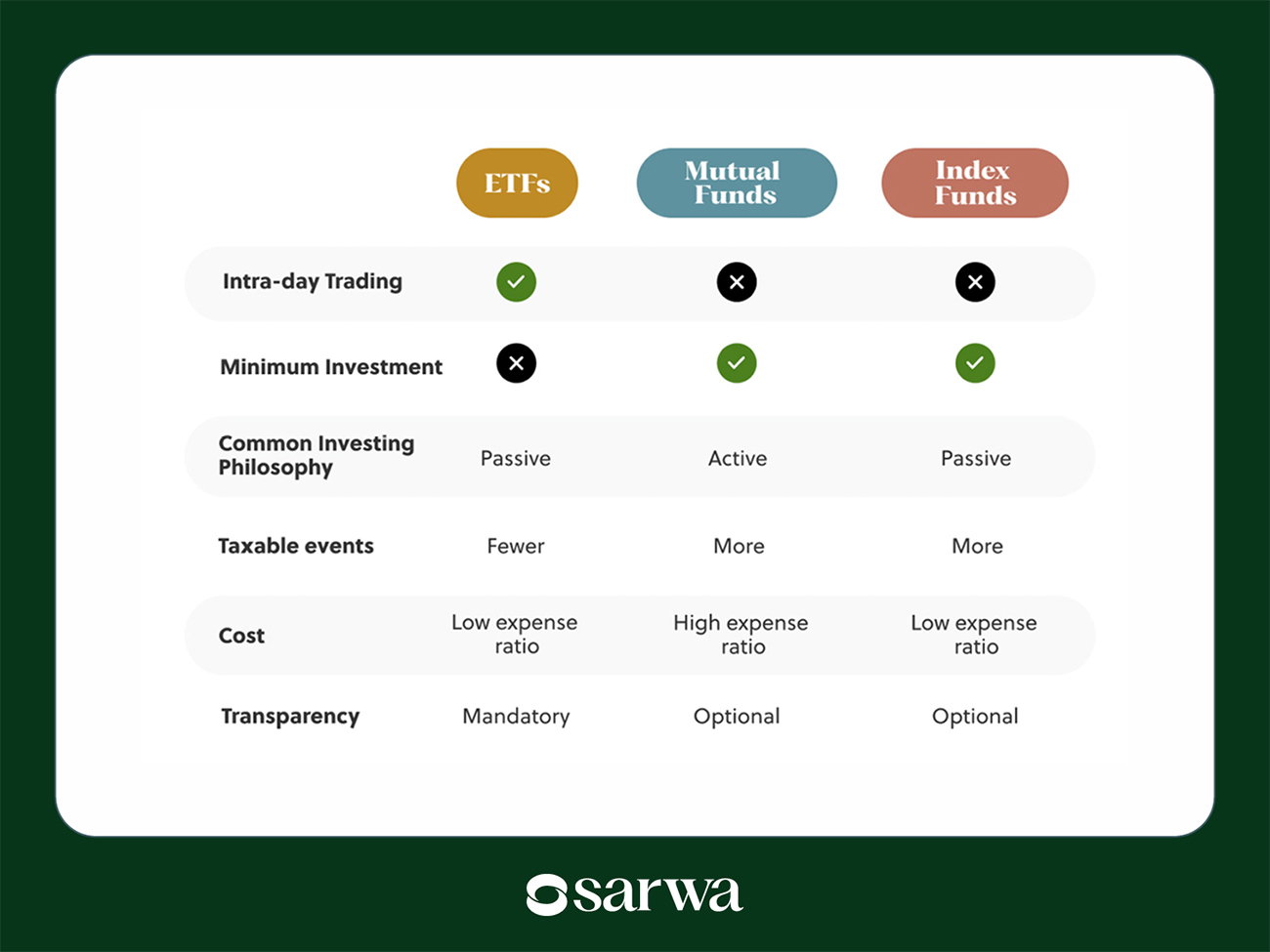

There are two popular ways to invest in the S&P 500 Index: index funds and ETFs.

Why invest in ETFs instead of index funds?

Index funds are passively managed mutual funds, so you can only trade them at the end of the trading day. On the other hand, ETFs are traded, like stocks, during normal trading hours, which means more liquidity.

Also, ETFs are more transparent than index funds as they are required to regularly disclose their holdings.

You can see more of these differences in the chart below:

So, one way to execute a SIP is to buy an S&P 500 ETF like VOO, SPY, IVV.

Now, let’s see how consistent investing in a SIP that consists of only an S&P 500 ETF can help you build wealth.

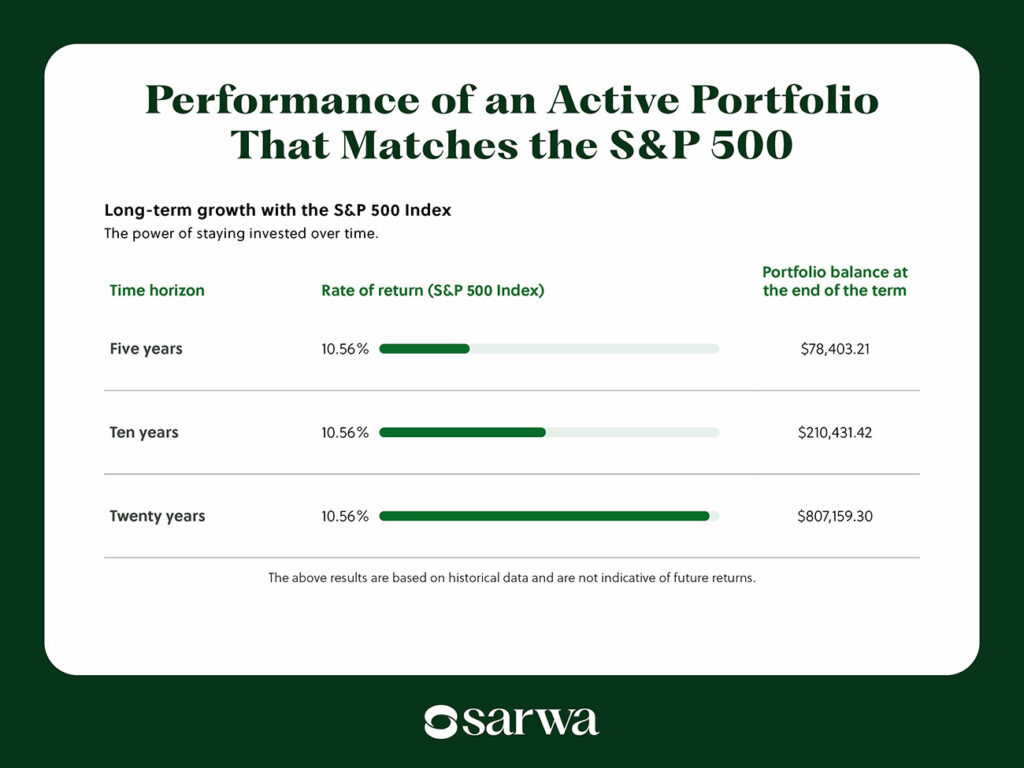

Between 1957 and 2025, the S&P 500 Index produced an average annual return of 10.56%, according to Investopedia, a financial education and research platform.

Of course, past performance does not guarantee future performance, and stocks are not fixed-income securities like fixed deposits or money market accounts.

Yet, past performance over a long period gives us a good picture of what we can expect in the future.

What then can you expect by consistently investing in the S&P 500 Index?

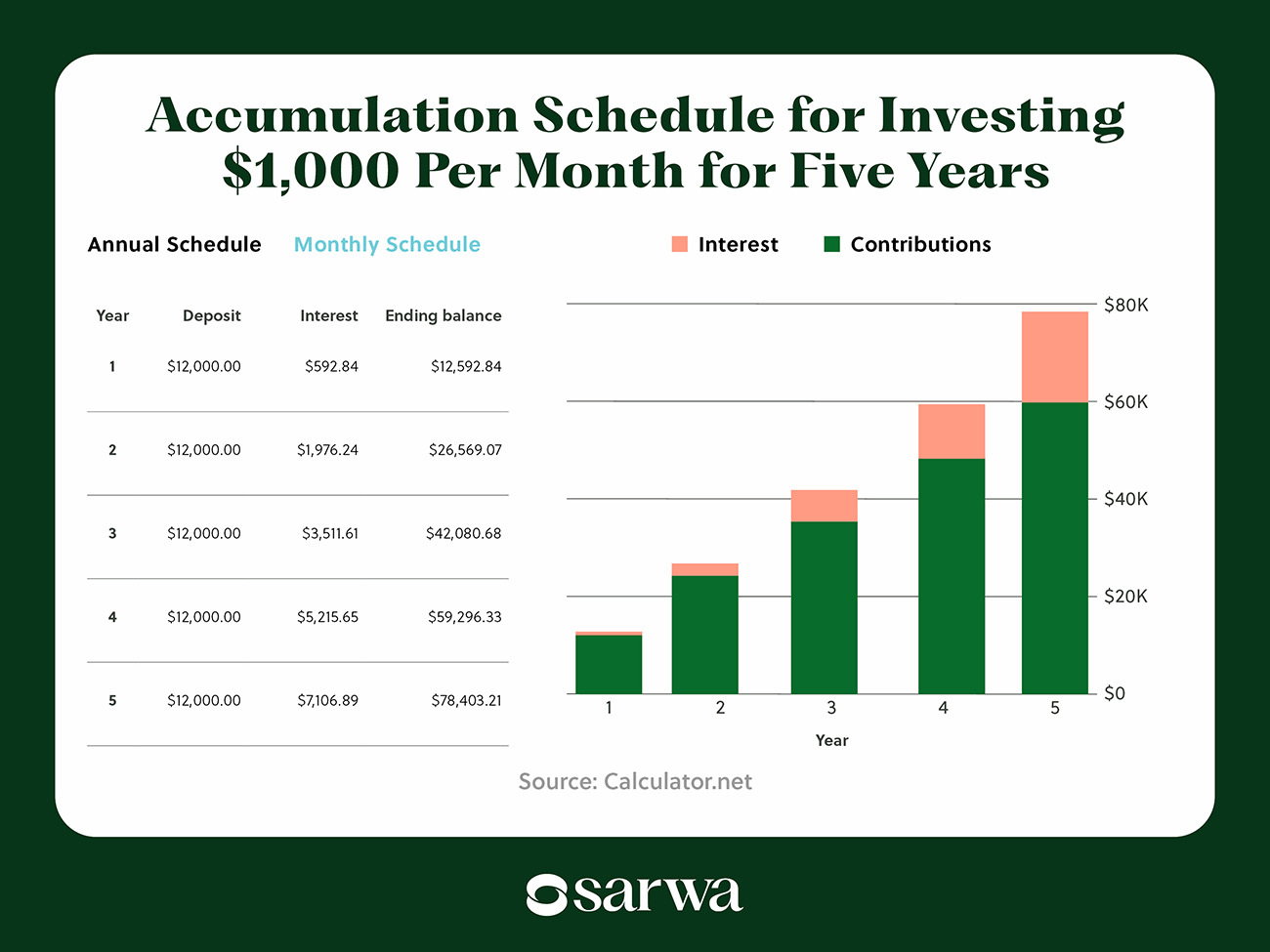

Invest $1,000 per month for 5 years

For these SIP calculations, we are using the following assumptions:

- $0 starting amount

- $1,000 invested at the end of every month

- An average annual return of 10.56%

- Quarterly compounding of interest paid into the portfolio (you reinvest dividends every 3 months)

- A 5-year investment period

Plugging these numbers into an investment growth calculator, you’ll have a portfolio worth $78,403.21 at the end of year 5.

Source: Calculator.net

Your contribution (total investment amount) is $60,000, while the market gives you free $18,403.21.

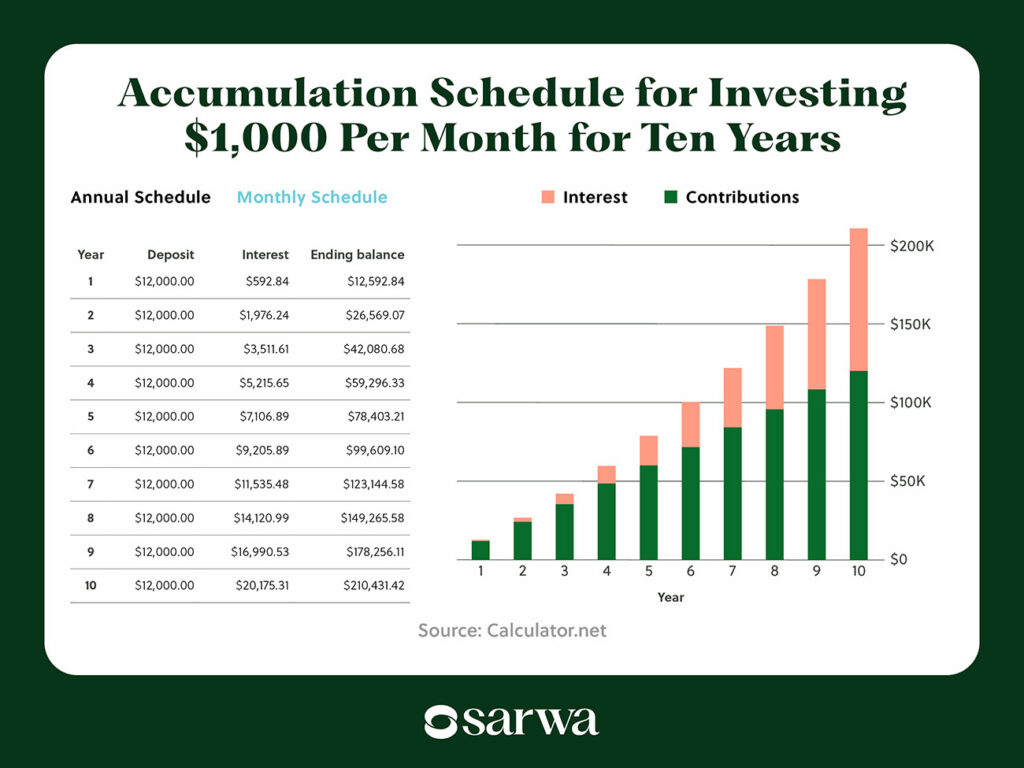

Invest $1,000 per month for 10 years

What if we use the same assumptions, except to extend the time horizon to ten years?

Now, your portfolio would be worth $210,431. 24.

Source: Calculator.net

This time, your contribution is $120,000, while the market gives you $90,431.42.

Notice that while your contribution over ten years is double what you would have contributed over five years, the free money you have for the ten-year scenario is 4.9X of what you would have gotten over five years.

The point? The more time you spend in the market, the more benefits you get from compound interest. Your free money grows geometrically, not arithmetically.

“Compounding works slowly, which is why people underestimate it,” according to Tapos Kumar, founder of Finance Ideas, a personal finance education website.

“In the early years, progress seems invisible, so many investors lose patience. But once consistency crosses a certain time standard, growth stops being linear and starts accelerating. Therefore, the lesson is not the amount invested; instead, it is how long the process is allowed to run uninterrupted.”

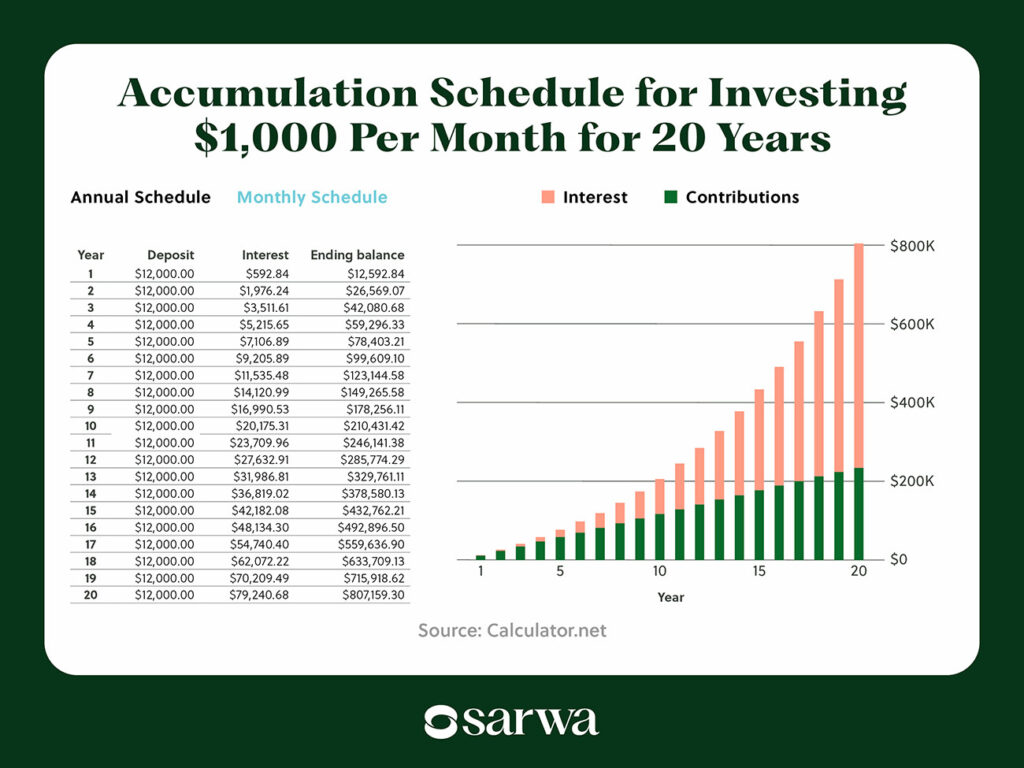

Invest $1,000 per month for 20 years

Let’s expand to 20 years.

This time, your portfolio would be worth $807,159.30, as seen below:

Source: Calculator.net

Notice again that while your contribution ($240,000) is now 4x of what it would have been over five years, the free money from the market ($567,159.30) is now 30.8X of what it would have been over five years.

Again, the more time you spend in the market, the more you gain from compounding.

The market can indeed be generous.

Investing with a digital wealth management advisor

Though investing in only the S&P 500 Index is generally considered good investment advice, especially for beginners, it might not be the best approach when market conditions change.

So, why not invest only in the S&P 500?

Expected return is an important component of investing, but so also is market risk.

Economic downturns and bear markets can cause the S&P 500 to deliver large losses over a given period.

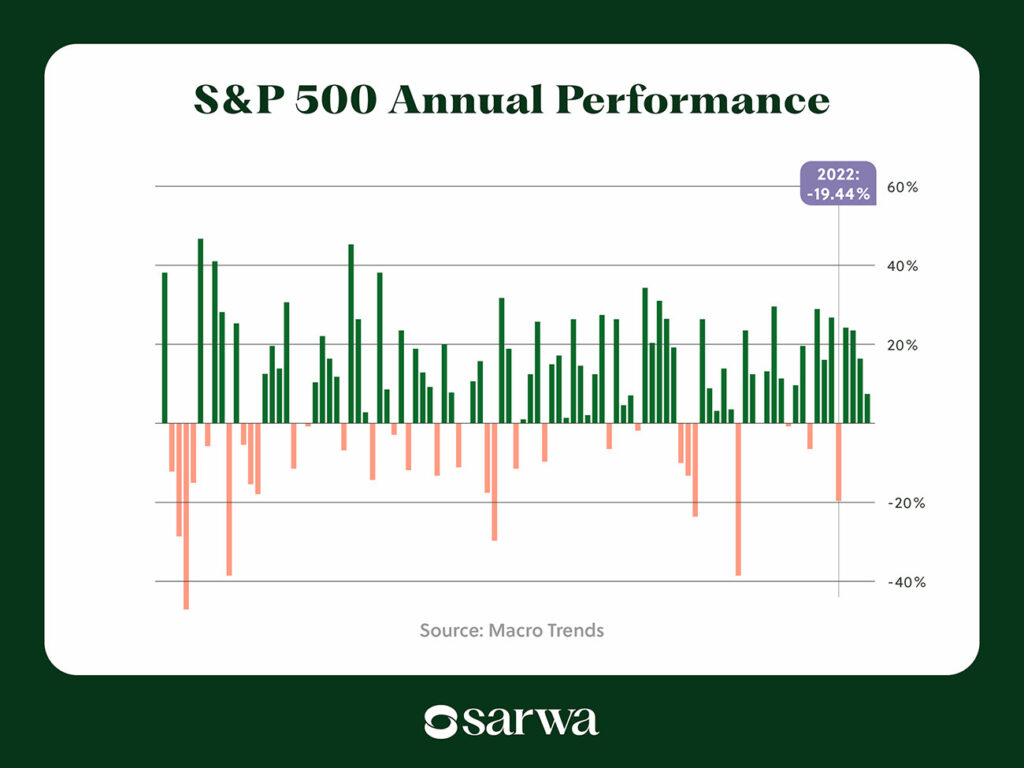

To take a recent example, the S&P 500 Index was down by 19.44% in 2022, as seen below, due to interest rate hikes, the Russia-Ukraine war, and lingering effects of the pandemic.

Source: Macro Trends

There are days, months, and years when the S&P 500 Index can be very volatile on the downside.

Though the market always recovers, this is only comforting if you have a long-term horizon to weather its storms. Consider someone who retired in January 2022 who had to deal with an almost 20% drop in their nest egg.

To avoid such situations, investors seek to diversify their portfolios with the best investment options in the UAE, like bonds, commodities, and real estate.

By adding other assets that are not highly correlated to the stock market, you can reduce your risk exposure and make it less likely to suffer a heavy blow when the stock market experiences dark days.

Also, the S&P 500 Index focuses solely on the US. But there are exciting markets outside of the US where you can earn higher returns (emerging markets) or lower but stable returns that can further reduce portfolio risk (developed markets ex-US).

Given the realities of geopolitical risk, such international diversification can be a good way to protect yourself from the geopolitical missteps of the US.

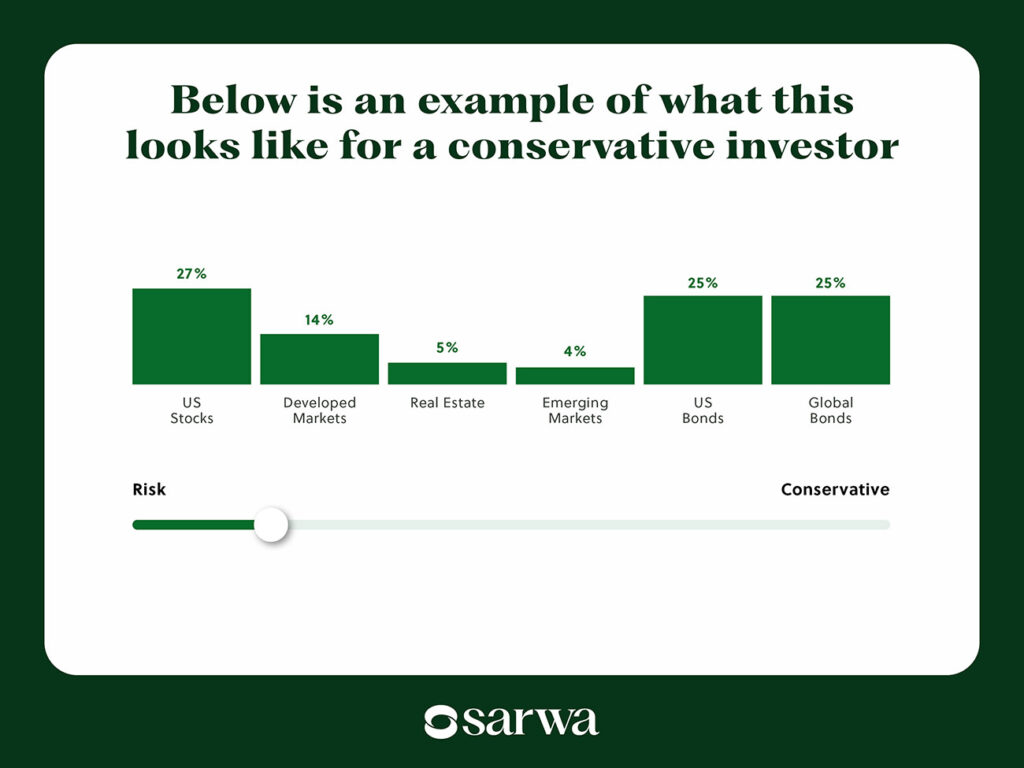

This is why, instead of buying only the S&P 500 ETF, some passive investors choose to invest with digital wealth management platforms (also called robo advisors) like Sarwa Invest.

These platforms will create a diversified, personalised portfolio of passive funds, such as exchange-traded funds (ETFs), that matches your risk appetite, investment goals, and time horizon.

With them, the situation where a retiree is losing 20% of their portfolio to the stock market will never happen. Someone with that time horizon would have a portfolio with a smaller percentage of stocks and a higher percentage of low-risk assets like bonds.

Invest $1,000 per month for 5 years

Given that digital wealth management platforms seek to provide a risk-return balance that matches your risk tolerance, time horizon, and investment goals, rather than maximising returns, the S&P 500 Index is not usually a benchmark.

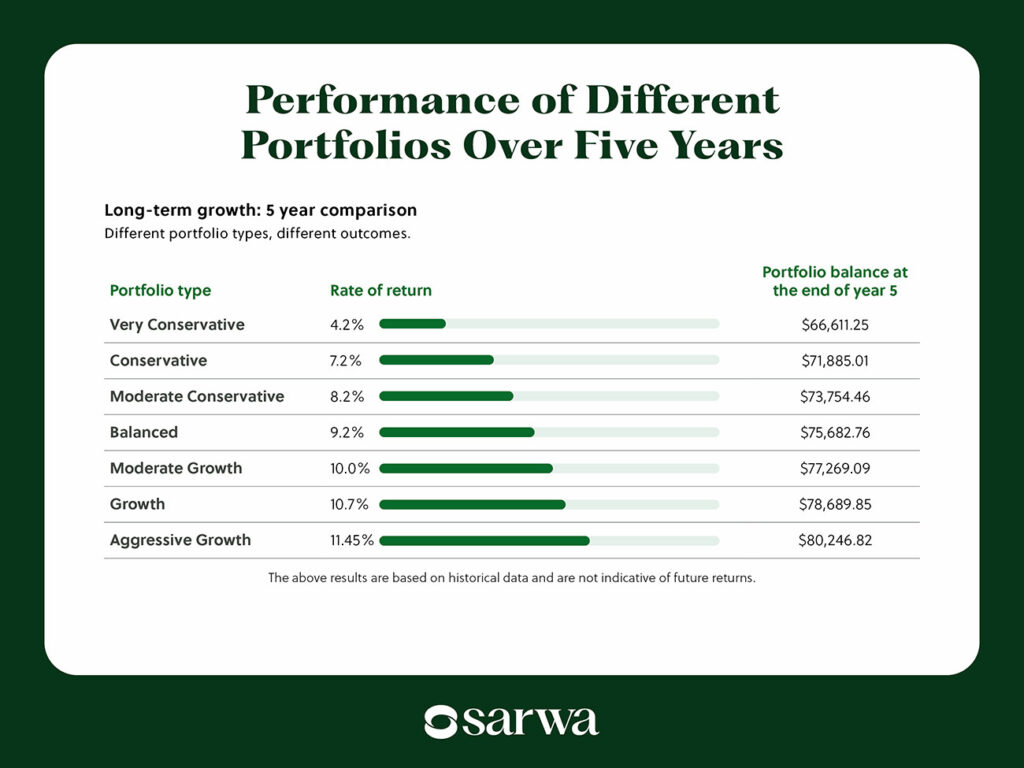

But we can still get a feel for what these platforms generate for investors with different risk profiles by considering the average return rate of different portfolios.

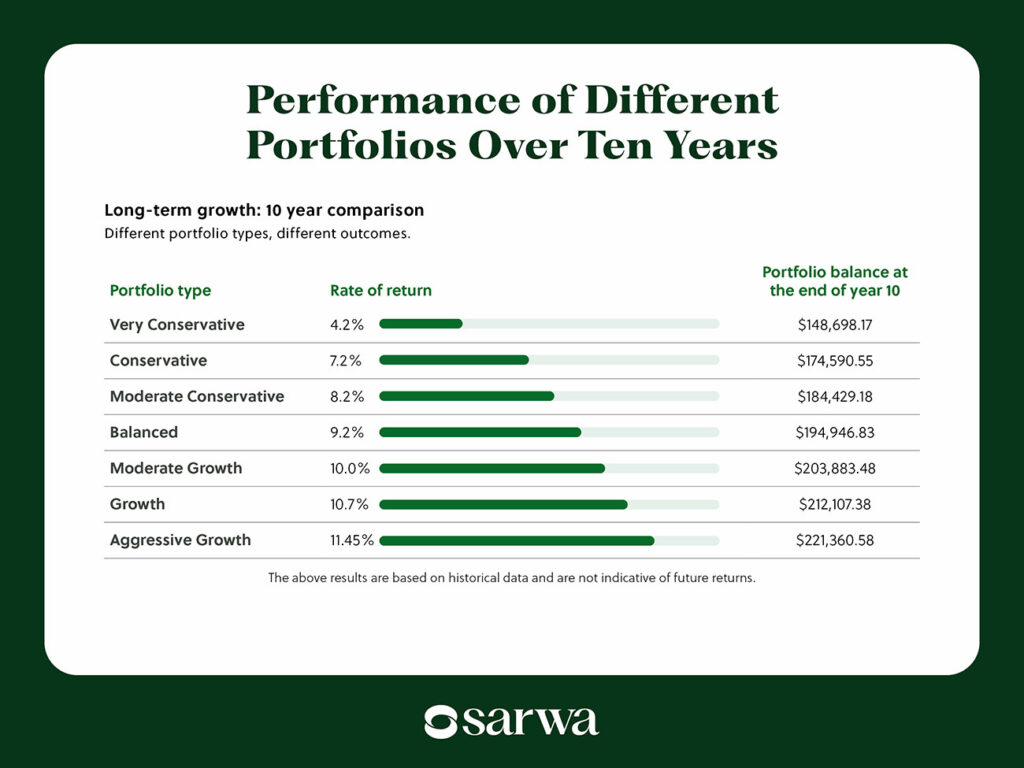

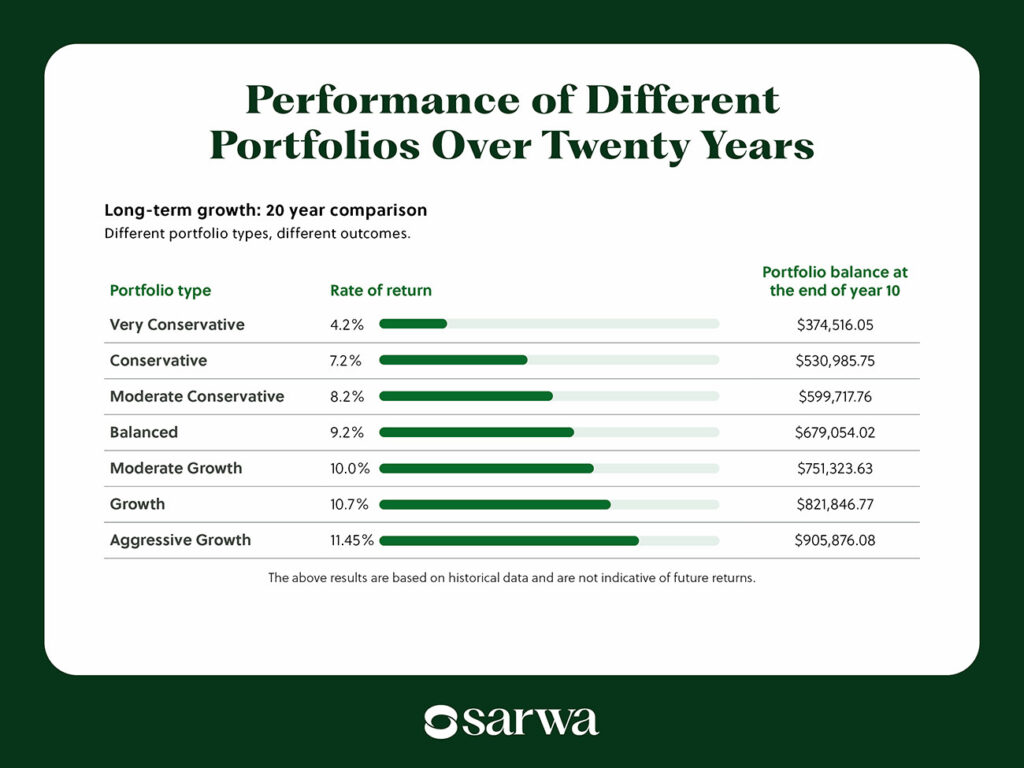

Below are the average annual returns (between December 2008 and December 2025) of the conventional portfolios offered by Sarwa Invest:

- Very Conservative: 4.2%

- Conservative: 7.2%

- Moderate Conservative: 8.2%

- Balanced: 9.2%

- Moderate Growth: 10%

- Growth: 10.7%

- Aggressive Growth: 11.45%

If we plug these numbers into the investment calculator as the potential returns for each portfolio (keeping the assumptions we made for investing in the S&P 500, except the rate of return), we get the following results:

Invest $1,000 per month for 10 years

Let’s see how these figures change if we extend the time horizon to ten years:

Invest $1,000 per month for 20 years

If we extend it to 20 years, we get even more fascinating results:

2. How consistent investing in a SIP builds wealth: Examples for active investors

If you have the time or expertise (in stock market fundamental and technical analysis), then you should consider building an investment portfolio from scratch.

In other words, you will select your assets and design an allocation formula that can help you achieve your goals.

Though we have said that many mutual fund investments (even with expert fund managers) underperform their benchmark indices, some of them still outperform (though whether they can do this consistently is another question).

In the same way, some individual investors have shown the ability to outperform the S&P 500 Index at times (even if not consistently).

If you believe you can do the same, nothing is stopping you from handling your own portfolio construction and management.

Though the passive vs active investment debate rages on, we believe that the best way to invest money depends on each individual, since you are the better judge of your ability.

If you do decide to go through the active route, Sarwa Trade has all the assets you need.

You can select passively-managed ETFs of stocks, bonds, REITs, gold, silver, and crude oil. Also, you can purchase individual stocks and even combine these with stock options and cryptocurrencies.

Since there is no guarantee that you would meet, exceed, or fall short of the S&P 500 Index, it is hard to project what your portfolio would look like in five, ten, or 20 years.

But since your goal is to exceed the performance of the S&P 500 Index, you can use the index as a benchmark of what happens if you invest $1,000 per month for five years, ten years, or twenty years.

As a reminder, this is what you can expect based on the historical performance of the S&P 500 Index:

3. How to construct and execute your SIP in the UAE

We have seen what happens if you invest $1,000 per month for five years, ten years, and 20 years.

One of the most important points we have noticed is that the market is generous. Knowing how to invest money to make money is all about knowing how to consistently invest in the market over the long term.

The best way to embrace this approach is to create a systematic investment plan in the UAE.

You can do this by following these simple steps:

- Have a budget: A budget helps you take control of your finances, and it is the foundation of sound personal finance.

The 50/30/20 rule is a popular one that you can adopt if you don’t have a budget.

- Decide on a monthly contribution as a percentage of your income: The 50/30/20 budget requires you to save and invest 20% of your income. What portion goes to saving or to investing depends on the interplay between your short-term and long-term financial goals.

Many financial planning experts would say a minimum of 10% is a good place to start. We have also seen people in the Financial Independence, Retire Early (FIRE) movement who have invested far more than that.

What matters most is consistency. Whether it’s 10% or 15%, do it consistently and you can be sure of building wealth over the long term.

Not everyone will have a lump sum from inheritance or employee stock options to invest in the market. But everyone can invest a portion of their monthly income, no matter how small it is.

“You don’t need a large sum of money,” said Jeff Zhou, the co-Founder and CEO of Fig, an alternative lending service. “The initial deposit can be the minimum, with monthly or quarterly deposits equaling 5% to 10% of your remaining budget after accounting for essential expenses. Baby steps are better than never taking the initial step.”

One further point: a percentage can be a better approach than a fixed amount. In this way, the SIP amount can grow as your income grows. This gives you more room to benefit from compounding.

- Choose an investment strategy and portfolio: We have considered three strategies you can explore: passive investing with only the S&P 500 ETF, passive investing with a digital wealth management platform, and active investing.

Choose the one that aligns best with your current situation and experience.

Once you have chosen a strategy, you need to build a portfolio of the best investment options in the UAE. This will be your wealth-generating vehicle.

- Automate investment into your portfolio: One of the ways to make it easier to invest than to overspend is to automate transfers from your checking or savings account to your investment account on your payday.

One of Warren Buffett’s quotes says you should spend what is left after saving. Automated investing is one way to do this.

It is also a way to enjoy the benefits of dollar-cost averaging instead of timing the market.

“SIPs (Systematic Investment Plans) remove time-sensitive influences from investor decision-making,” according to Rachel Sinclair, the acquisitions director at US Gold and Coin, a network of precious metals buyers. “Small consistent payments into your retirement account buy more shares when the price is lower and fewer shares when it’s higher. Investment buying costs are smoothed out by SIPs. SIPs let you create wealth consistently with no surprises because compound interest builds quietly over time.”

- Automate dividend/interest reinvestment: One of the assumptions we made in the calculations above is that you will be reinvesting your dividends every quarter.

If you are investing with a platform like Sarwa Invest, you can automate this process. With Sarwa Trade, you can choose to reinvest rather than withdraw your dividends (and interest) when they arrive.

- Monitor performance: If you invest with Sarwa Invest, you will get regular performance reports. You can also monitor your actively managed portfolio on Sarwa Trade. Sarwa provides you with enough information to understand your performance.

However, building wealth through a SIP is a marathon. It is not enough to know how to invest $1,000 in stocks; you must stick to it over the years.

“My personal experience has shown me that the size of your contribution means nothing compared to how long you contribute,” according to Mike Roberts, co-founder of City Creek Mortgage, a mortgage broker. “I contributed small sums of money, but I looked at these contributions as expenses – just like paying a mortgage payment.”

There will be days, weeks, and months when volatility heightens (irrespective of the strategy you choose). You must have the patience to weather the short-term fluctuations in pursuit of long-term wealth.

Also, many people get discouraged when they check their portfolio after a few weeks or months, and the growth seems insignificant. Understand that only those who can wait it out during the boring days will enjoy the wealth that accumulates over the years.

“It is hard to see results in the early years,” according to Des Cooney, a financial consultant at Axis Financial Consultants, a financial consultancy firm. “Later, growth may be much more prominent since the portfolio has had more time to grow. That’s why it’s so important to be in the market for a long time. An individual who begins saving in their 20s or 30s with $100 or $200 per month could end up in a better position than a person who waits until they receive a higher wage, because they have lost 15 years of compounding.”

If you are ready to start your wealth-building journey in the UAE, Sarwa is the partner you need.

We provide you with various products that can help you execute both a passive and an active investment strategy.

In support of your investment goals, we also provide you with educational resources that can make you a better investor and personalised customer support that makes it easier for you to use our platform.

We also protect your data and money with our bank-level cybersecurity. Finally, we make your investment cost-effective by providing free transfers from (and to) your bank accounts to your brokerage accounts, charging low commissions, and ensuring there are no hidden fees.

Are you ready to start investing to build wealth? Sign up today for Sarwa for cost-effective, seamless, and secure investing in the UAE. Don’t know how to start? Schedule a free call with a Sarwa wealth advisor.

Takeaways

- Consistent investing beats get-rich-quick schemes and helps investors build wealth steadily over time.

- Investing $1,000 monthly in an S&P 500 ETF could grow to over $807,000 in 20 years through compounding.

- Passive investing through ETFs or robo advisors offers diversification, lower fees, and long-term growth potential.

- The secret to wealth creation is not timing the market but staying invested consistently for years.